MUMBAI: Buyout groups Brookfield and EQT are in active discussions to buy Hyderabad-based Gland Pharma, a contract development and manufacturing organisation (CDMO) and injectables company, from China’s Fosun Group in what could become one of the largest buyouts of the year in the segment, said people in the know. However, the galloping share price of Gland is a potential deal spoiler.

The two PE groups have been shortlisted after the initial round of bids earlier this month.

Others such as CVC Capital Partners are also exploring a deal, said the people cited. Warburg Pincus is said to be weighing its options before taking a call, they said.

The Chinese parent has diversified investments that range from healthcare to football clubs, asset management, banks, estate, hospitality, fashion and industrials. The conglomerate has a presence across the pharma value chain from manufacturing to diagnostics and medical devices. Shanghai Fosun Pharmaceutical Co. had acquired an 86% stake in Gland Pharma in 2016 from KKR for a record deal value of $1.26 billion.

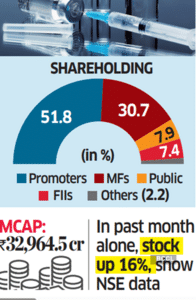

Fosun currently owns 51.8% of Gland, having pared its stake over the years. Market capitalisation has shot up to Rs 32,964.47 crore with the Gland Pharma stock appreciating 10% in the year to date in anticipation of a transaction. It closed Friday at Rs 2,000. In the past month alone, it has shot up 16%. The Fosun stake alone would require a payout of Rs 17,141.28 crore ($1.9 billion).

Change of control will involve an open offer for an additional 26% of the company from minority shareholders, making it a much larger transaction. If the open offer is fully subscribed, it would translate to a Rs 25,711 crore ($3 billion) acquisition at current prices.

Fosun and Gland didn’t respond to queries. Brookfield and EQT declined to comment.

Most investors are of the view the stock is overpriced and are interested only at a discount to the current level.

“There are macro headwinds because of industry glut and geopolitics,” said one of the people cited. “Fosun has to decide if it is okay to sell at a significantly lower price.”

This factor could be a deal breaker, analysts said.

“At this level, the process looks tough,” said another industry official.

Fosun at various times in recent years, renewed its search for a strategic or financial deal for Gland Pharma. The company ran a full sale process last year but aborted it, only to revive plans earlier this summer, mandating Morgan Stanley and UBS.

Mint was first to report that PE interest in Gland had revived in February.

Founded in 1978 by PVN Raju, Gland Pharma develops and manufactures generic injectables for use in nearly 90 countries on five continents, with a focus on the Indian and US markets.

As with other Chinese companies, Fosun has faced regulatory issues in India due to the frosty relationship between the two countries. Even its entry into India faced significant delays with deal contours needing tweaks to comply with FDI norms. Some experts said Fosun sees the timing as ideal for an exit. But with no success for years, Fosun has been selling down its shares in the public markets through block deals. Last year, it sold about 6% for Rs 1,750 crore.

“The incremental growth for the company’s base business in the US is likely to come at the cost of margins,” said Shyam Srinivasan of Goldman Sachs.

The management is expecting Cenexi Group — a French injectables and CDMO company Gland acquired in 2023 — to break even by the December quarter. Gland has a toehold in Europe through Cenexi, but rebooting the organisation and its product mix has been tough.

Some analysts said Gland has a sound track record and its future prospects may attract buyers.

A veteran industry expert said Gland Pharma has a “strong compliance history” and its manufacturing quality is impeccable. Plus, a surge in demand is seen for large injectable capacities across the world, making it a good fit. Another strong push for Gland Pharma is the explosive growth in glucagon-like peptide-1(GLP-1) drugs for weight loss and diabetes. Novo Nordisk’s Wegovy (semaglutide) is set to go off patent early next year in India and Canada, leading to a burst of generic variants expected to enter the market. This is likely to offset the current overcapacity of injectable assets around the world.

Trade tensions between the US and China are adding to the interest in Indian contract manufacturing players for steady supplies.

“Although we have not seen any meaningful switching from China yet, such opportunities cannot be ruled out in the future,” an industry executive said.

In its investor presentation in May this year, Gland Pharma hinted at that possibility. The company launched its first partnered GLP-1 (liraglutide) in the fourth quarter of FY25, secured two contracts and discussions are ongoing with several other partners. Investments are being made to increase the current GLP-1/pen/cartridge capacity of 40 million to 140 million.

Gland is also preparing for a larger play in the biologics business, focusing on expanding its biosimilar and biologic CDMO segment.

“The company's collaboration with DRL (Dr Reddy’s) and discussions with Henlius (of China) are progressing well, with revenue generation from DRL business expected from FY26,” it said in the presentation. Gland posted FY25 revenue of Rs 5,616 crore with an after-tax profit of Rs 698 crore.

With opportunities unfolding, private equity players are lapping up CDMO businesses in key geographies. On July 18, EQT announced it acquired Adalvo, an asset-light dossier developer for generic companies based in Malta for an undisclosed amount. In India, private equity firm Advent International has invested about $2 billion in buying a string of companies over the last five years and clubbing them under the umbrella CDMO brand Cohance Lifesciences.

The two PE groups have been shortlisted after the initial round of bids earlier this month.

Others such as CVC Capital Partners are also exploring a deal, said the people cited. Warburg Pincus is said to be weighing its options before taking a call, they said.

The Chinese parent has diversified investments that range from healthcare to football clubs, asset management, banks, estate, hospitality, fashion and industrials. The conglomerate has a presence across the pharma value chain from manufacturing to diagnostics and medical devices. Shanghai Fosun Pharmaceutical Co. had acquired an 86% stake in Gland Pharma in 2016 from KKR for a record deal value of $1.26 billion.

Fosun currently owns 51.8% of Gland, having pared its stake over the years. Market capitalisation has shot up to Rs 32,964.47 crore with the Gland Pharma stock appreciating 10% in the year to date in anticipation of a transaction. It closed Friday at Rs 2,000. In the past month alone, it has shot up 16%. The Fosun stake alone would require a payout of Rs 17,141.28 crore ($1.9 billion).

Change of control will involve an open offer for an additional 26% of the company from minority shareholders, making it a much larger transaction. If the open offer is fully subscribed, it would translate to a Rs 25,711 crore ($3 billion) acquisition at current prices.

Fosun and Gland didn’t respond to queries. Brookfield and EQT declined to comment.

Most investors are of the view the stock is overpriced and are interested only at a discount to the current level.

“There are macro headwinds because of industry glut and geopolitics,” said one of the people cited. “Fosun has to decide if it is okay to sell at a significantly lower price.”

This factor could be a deal breaker, analysts said.

“At this level, the process looks tough,” said another industry official.

Fosun at various times in recent years, renewed its search for a strategic or financial deal for Gland Pharma. The company ran a full sale process last year but aborted it, only to revive plans earlier this summer, mandating Morgan Stanley and UBS.

Mint was first to report that PE interest in Gland had revived in February.

Founded in 1978 by PVN Raju, Gland Pharma develops and manufactures generic injectables for use in nearly 90 countries on five continents, with a focus on the Indian and US markets.

As with other Chinese companies, Fosun has faced regulatory issues in India due to the frosty relationship between the two countries. Even its entry into India faced significant delays with deal contours needing tweaks to comply with FDI norms. Some experts said Fosun sees the timing as ideal for an exit. But with no success for years, Fosun has been selling down its shares in the public markets through block deals. Last year, it sold about 6% for Rs 1,750 crore.

“The incremental growth for the company’s base business in the US is likely to come at the cost of margins,” said Shyam Srinivasan of Goldman Sachs.

The management is expecting Cenexi Group — a French injectables and CDMO company Gland acquired in 2023 — to break even by the December quarter. Gland has a toehold in Europe through Cenexi, but rebooting the organisation and its product mix has been tough.

Some analysts said Gland has a sound track record and its future prospects may attract buyers.

A veteran industry expert said Gland Pharma has a “strong compliance history” and its manufacturing quality is impeccable. Plus, a surge in demand is seen for large injectable capacities across the world, making it a good fit. Another strong push for Gland Pharma is the explosive growth in glucagon-like peptide-1(GLP-1) drugs for weight loss and diabetes. Novo Nordisk’s Wegovy (semaglutide) is set to go off patent early next year in India and Canada, leading to a burst of generic variants expected to enter the market. This is likely to offset the current overcapacity of injectable assets around the world.

Trade tensions between the US and China are adding to the interest in Indian contract manufacturing players for steady supplies.

“Although we have not seen any meaningful switching from China yet, such opportunities cannot be ruled out in the future,” an industry executive said.

In its investor presentation in May this year, Gland Pharma hinted at that possibility. The company launched its first partnered GLP-1 (liraglutide) in the fourth quarter of FY25, secured two contracts and discussions are ongoing with several other partners. Investments are being made to increase the current GLP-1/pen/cartridge capacity of 40 million to 140 million.

Gland is also preparing for a larger play in the biologics business, focusing on expanding its biosimilar and biologic CDMO segment.

“The company's collaboration with DRL (Dr Reddy’s) and discussions with Henlius (of China) are progressing well, with revenue generation from DRL business expected from FY26,” it said in the presentation. Gland posted FY25 revenue of Rs 5,616 crore with an after-tax profit of Rs 698 crore.

With opportunities unfolding, private equity players are lapping up CDMO businesses in key geographies. On July 18, EQT announced it acquired Adalvo, an asset-light dossier developer for generic companies based in Malta for an undisclosed amount. In India, private equity firm Advent International has invested about $2 billion in buying a string of companies over the last five years and clubbing them under the umbrella CDMO brand Cohance Lifesciences.

You may also like

India's GDP to grow at 6.5 pc this fiscal, inflation to soften at 4 pc on average: Crisil

Lok Sabha adjourned within first 20 minutes: Ruckus in Parliament on first day of Monsoon session; oppn MPs raise slogans

SC refuses urgent listing of plea seeking FIR against Allahabad HC judge in cash discovery row

Man Utd transfer news LIVE: Gyokeres hijack, Mbeumo announcement, Chelsea swap deal

Rachel Booth missing: Everything we know as new clues emerge after mum vanishes